RCM - Reverse Charge Mechanism (GST - Goods & Services Tax)

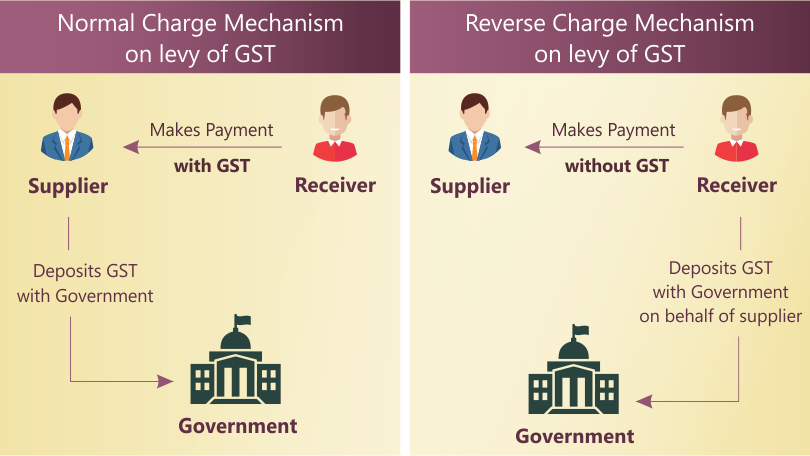

Forward Mechanism: Typically, the supplier of goods or services pays the tax on supply. That is, the Purchaser makes payment (with GST) to the Supplier and the Supplier will deposit the GST with the Government.

In RCM, The recipient (i.e., purchaser) of goods or services becomes liable to pay the tax, i.e., the chargeability gets reversed. Here, the Purchaser makes payment (without GST) to the Supplier and it is the responsibility of the Purchaser to deposit the GST with the Government on behalf of the Supplier.

In Indian Railways - GST

Forward mechanism: Services relating to passenger and freight service and any other service rendered to unregistered persons only

IR registered under GST as Central Government though it is a business entity. IR has 36 registrations and each State and UT has been assigned with a Nodal Officer.

Transportation of passengers & Goods are the two principal outward supplies of Services. Railways as a Supplier is responsible to deposit GST with the Government.

Taxable: Non AC First Class and AC classes - GST Rate is 5%

Non Taxable: 1. Sleeper class (Non AC) 2. General Class 3. Relief materials 4. Newspapers 5. Railway materials 6. Agricultural products, Milk, Salt, Food grains & organic manure.

RCM - Reverse Charge Mechanism: Railway as a Receiver is responsible to deposit GST with the Government. Examples are: Land licensing, Parking Contracts, renting out of immovable properties, way leave charges.