Material At Site A/c – M A S

·

Source: 1436 Engineering Code

·

It is one of the Suspense heads operated on

erstwhile Demand No. 16

·

M A S A/c records the stores obtained for

specific works.

·

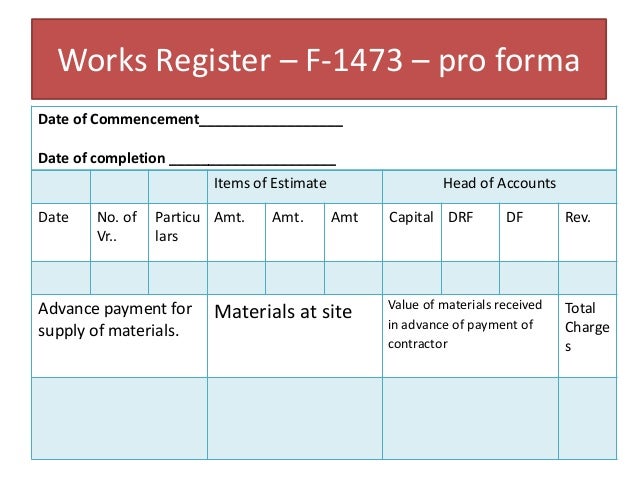

MAS A/c shown as last

but two column in the Works Register.

(Last column is Total Charges, Last but one column is value of material recd in

advance of payment to contractors, last but third

column is Advance payment for supply of materials)

·

For materials obtained for specific works,

received at the site of the work and not immediately consumed on the works

should be temporarily held at charge of a sub-head of work under

“Material-at-Site Account” in the Register of Works.

·

Material obtained for specific works

should be kept outside the accounts of any other category of stores. Such material,

be deemed to be “Material At Site”

·

MAS A/c – To be maintained for works valuing Rs. One lakh and for

Track Renewal works valuing Rs. 3 Lakhs.

·

Maintained by Executive in charge of the work.

·

Custody of Materials under MAS – either under the custody of the

in charge of Work or kept in Engineering Stores Depot under the custody of

DMS/DSK

·

Minus Issues: Releasing material from

works and Material so issued, but found subsequently to be surplus. (Not as

Receipts)

·

Minus Receipts : Material returned to Stores or transferred to other works. (not

as Issues)

·

Executive is responsible for 1. Daily numerical record 2.

Monthly return

%%%%